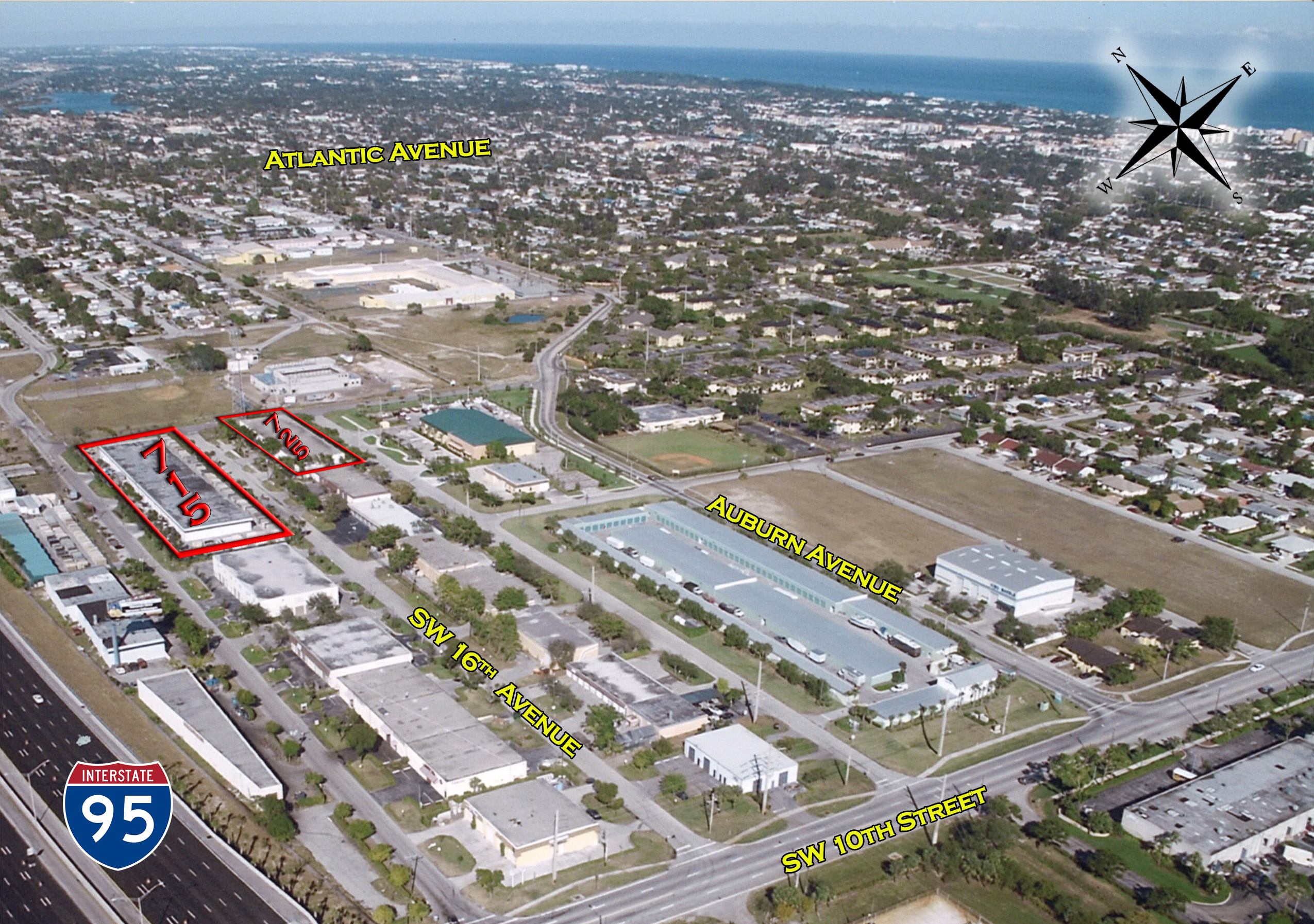

Tom Robertson, Senior Managing Partner with CRE Rauch Lupo Robertson, CRE Florida Partners Company, recently completed the sale of an industrial property located at 3411 SW 11th Street in Deerfield Beach.

Sand & Steel Properties LLC purchased the asset for $1,840,000 or $86.94 per square foot.

Sand & Steel Properties LLC purchased the asset for $1,840,000 or $86.94 per square foot.

The 21,165-square-foot facility, which is situated on 1.3 acres, was built in 1987 and fronts on both 10th and 11th Street.

“The property’s close proximity to Sawgrass Expressway and I-95 via SW 10th Street certainly added tremendous value to the offering,” said Robertson. CRE Florida Partners is currently working with several buyers looking for 20,000 – 40,000 SF Industrial buildings in Broward and Palm Beach County.

Tom Robertson

Robertson, who represented the leasing interests for the property on behalf of the seller, 3411 Building LLC, since 2002, represented the seller in the transaction.

“This transaction is one of the best examples I’ve seen of the way our firm handles long term relationships with our clients. Tom managed this property through lease up and sale with skill and patience,” added CRE Rauch Lupo Robertson Senior Managing Partner Michael Rauch.